Quick Wins To Increase Merchant Onboarding For European Payments Companies

Try the platform

Share the article

Merchant onboarding is one of the most critical, and complex, functions in a payments company’s operations. It is essential for ensuring regulatory compliance and enabling merchants to quickly begin processing payments. Yet for many payments companies, merchant onboarding remains slow, fragmented, and overly manual.

Lengthy back-and-forths, document collection, identity verification, and risk assessments are often handled across disconnected systems and teams. The result? Delays in merchant activation, increased risk of human error, and a higher likelihood of merchant churn.

To remain competitive, payments companies must be able to offer a fast onboarding experience. Achieving this at scale requires automation. Provided with the right infrastructure, payments companies can optimize onboarding and improve conversion rates.

This report covers how automation can drive immediate improvements in merchant onboarding (briefly touching upon the onboarding of merchant owners, too), finishing with a cheat sheet of non-negotiable best practices.

The Merchant Onboarding Saga

Merchant onboarding is fundamentally more complex than individual onboarding. Payments companies must verify the legitimacy of the business, identify and authenticate beneficial owners (UBOs), assess business risk, screen for prohibited categories, and validate bank account details — often across multiple jurisdictions. Traditional onboarding involves:

Doing this manually slows down time-to-revenue and increases the likelihood of errors, inconsistent reviews, and regulatory gaps.

But what if you could achieve two goals at once? Namely, with the right automation tool, you can both increase automated merchant onboarding, as well as facilitate a more optimized compliance process – without hindering security or user experience. That’s what will be explored in detail further down this report. First, a closer look at the regulatory landscape impacting payments onboarding across Europe.

Merchant Owner Onboarding

Whilst merchant onboarding is the operational core of many payments companies, there is also a need to support onboarding processes specifically for the owners of merchant businesses. This extends beyond traditional onboarding to include verification and due diligence for individuals who control or have ownership of the business entity. These onboarding processes typically involve:

- Electronic ID verification (eIDV)

- Biometric document verification (passport, ID cards)

- PEP/sanctions screening for individuals

- Risk scoring for fraud detection and onboarding approval

Optimizing these flows enhances compliance and reduces friction – and many of the same automation principles used for merchants can also be applied here.

Process Optimization for Onboarding Merchants & Merchant Owners

Automating onboarding across both merchant and owner segments involves streamlining key touchpoints:

Reduce Friction in Identity and Business Verification

- Use digital registry APIs to auto-populate business data

- Apply eIDV and biometric checks for UBOs and individuals

- Leverage pre-filled forms to reduce user input

Automate AML and Risk Scoring

- Integrate real-time screening against global sanctions/PEP lists

- Use risk models tailored to business type, transaction volume, and geography

- Auto-flag high-risk merchants for enhanced review

Enhance the Onboarding Experience

- Pre-fill data from identity sources and KYB registries

- Enable multi-language onboarding flows

- Use e-signatures and automated approvals to accelerate time-to-live

Best Practices for Automated Merchant Onboarding: A Quick Win Checklist

1. Streamline Business Verification:

- Automate identity checks using spektr's digital workflows.

- Extract and verify UBOs from uploaded documents or external databases.

2. Automate Compliance Processes:

- Leverage spektr's built-in AML and PEP screening workflows.

- Configure rule-based risk scoring and escalations for high-risk merchants.

3. Enhance User Experience:

- Create smooth onboarding flows with customizable templates in spektr.

- Support multiple entity types, languages, and jurisdictions.

4. Optimize Operational Efficiency:

- Use spektr's automated workflows to reduce manual data entry.

- Centralize compliance data and reporting in one interface.

What else can you expect when using spektr?

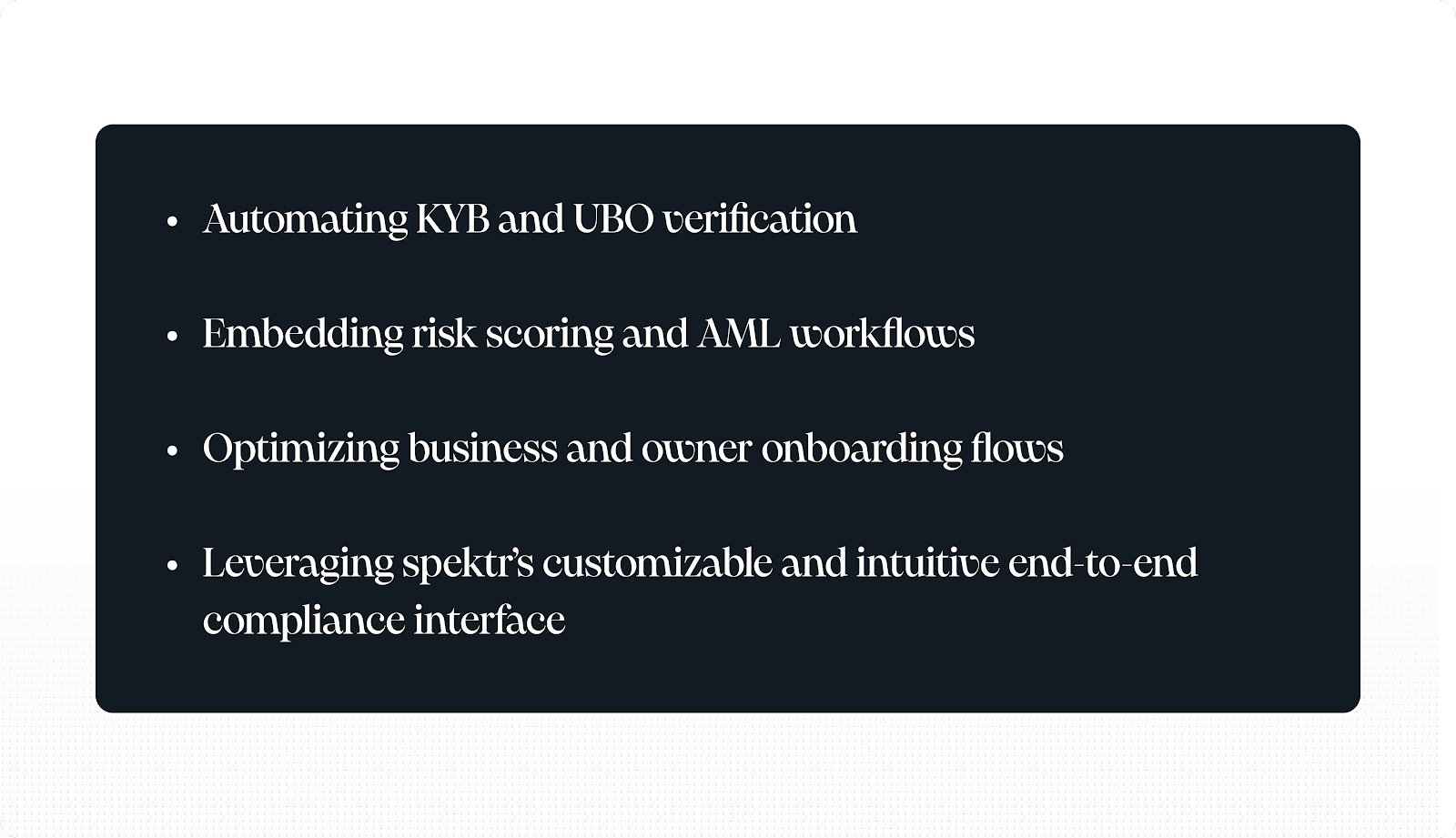

- End-to-end workflow automation: From KYB and UBO verification to approvals and case resolution.

- Customizable onboarding interfaces: A customizable interface makes it easier for merchants to navigate through onboarding flows. Furthermore, when it comes to building your onboarding flow, you can fully personalize features such as fonts, colors, logos etc.

- Case management and risk oversight: Gain clarity on every case so you can prioritize with precision and resolve any issues quickly in one place.

- API-driven Integrations: Instantaneously sync with your existing CRM, payment gateway, or underwriting tools.

spektr offers an end-to-end compliance solution that helps speed up onboarding processes, as well as automating everything else that follows, including monitoring and alert resolution. Scaling compliance operations manually is challenging, which is why a tech-driven approach that minimizes errors is essential.

spektr is a team composed of individuals from compliance, legal, tech, and finance backgrounds – ensuring the expertise needed to navigate complex onboarding and regulatory requirements.

Regulatory Frameworks & Compliance Considerations Across Europe

The following section breaks down key KYC and AML requirements for a handful of different countries across Europe to illustrate how onboarding may be impacted. But before jumping into the country-specific rules and regulations, what are some overarching compliance requirements that payments companies should be aware of?

- PSD2: Governs payments-related services, requiring strong controls over onboarding processes, particularly for agents and merchants.

- EBA Guidelines: Emphasize secure, risk-based identity verification and due diligence tailored to business entities.

- EU AML Directives (AMLD): The EU’s Anti-Money Laundering Directives define UBO requirements, enhanced due diligence, and ongoing monitoring obligations.

Conclusion

To scale operations and activate merchants faster, it is beneficial for payments companies to prioritize investing in their onboarding infrastructure. Ultimately, payments companies must be able to offer an intuitive and frictionless experience to merchants and merchant owners. Constant back-and-forth communications and adhering to a strictly manual approach will cost time and resources. That’s why this guide was designed to cover just some of the key ways to automate the process of merchant onboarding.

Key strategies include:

By adopting tech-driven solutions, payments companies can accelerate onboarding, enhance compliance, and improve conversion rates. Interested in learning more about how spektr can help you with automating your onboarding? Set up a chat with one of our pros. If you’re also just interested in learning more about best practices and different regulations globally, our in-house legal team can keep you updated.